4 Best Practices for Nonprofit Year-End Financial Management

By Jon Osterburg of Jitasa

The end of the year is a busy time for nonprofit teams. While exact numbers vary, it’s generally agreed that somewhere between one fourth and one third of annual charitable giving in December. So, your fundraising efforts from GivingTuesday through December 31 are critical for helping your organization achieve its annual goals and go into the new year fully funded.

However, fundraising shouldn’t be your only priority at year-end. Especially if your organization’s fiscal year follows the calendar year (as most nonprofits’ do), there are several essential financial management tasks you’ll need to take care of during this season. And as Jitasa’s year-end giving guide points out, “While you might treat fundraising and financial management as separate tasks, they need to work together for the best possible results.”

In this guide, we’ll walk through four best practices for managing your nonprofit’s finances at year-end and discuss how they align with your fundraising efforts. Let’s get started!

1. Review & Update Your Chart of Accounts

Your chart of accounts (COA) serves as a directory of your nonprofit’s financial records. Since this resource is the backbone of all of your organization’s accounting procedures, reviewing it in depth at least once a year will help you ensure it stays up to date and is as useful as possible to your team’s decision-making.

Most nonprofit COAs have the following main sections:

Assets: What your organization owns, including cash, property, and accounts receivable.

Liabilities: What your nonprofit owes, such as debt, deferred revenue, and accounts payable.

Net Assets: What your organization is worth, calculated by subtracting your total liabilities from your total assets.

Revenue: All of the funding your nonprofit receives from individual donations, corporate philanthropy, earned income, investment returns, and grants.

Expenses: All of the money your organization spends on its mission-related programs, administrative needs like staff compensation and utility bills, and the upfront costs of fundraising campaigns.

These categories are based on the Unified Chart of Accounts (UCOA), a sample nonprofit COA that is useful for standardization but tends to be too complex for all but the largest organizations to copy. Your nonprofit will likely benefit most from using the UCOA as a guide to the types of accounts you might want to include on your COA from year to year.

During your year-end COA review, remove any accounts you haven’t used in the past year and don’t plan to use next year, and add any new costs or revenue streams you’re considering incorporating into your strategy. Then, reconcile the rest of your accounts with your investment and bank statements to ensure all transactions are correctly accounted for.

2. Compile Financial Statements

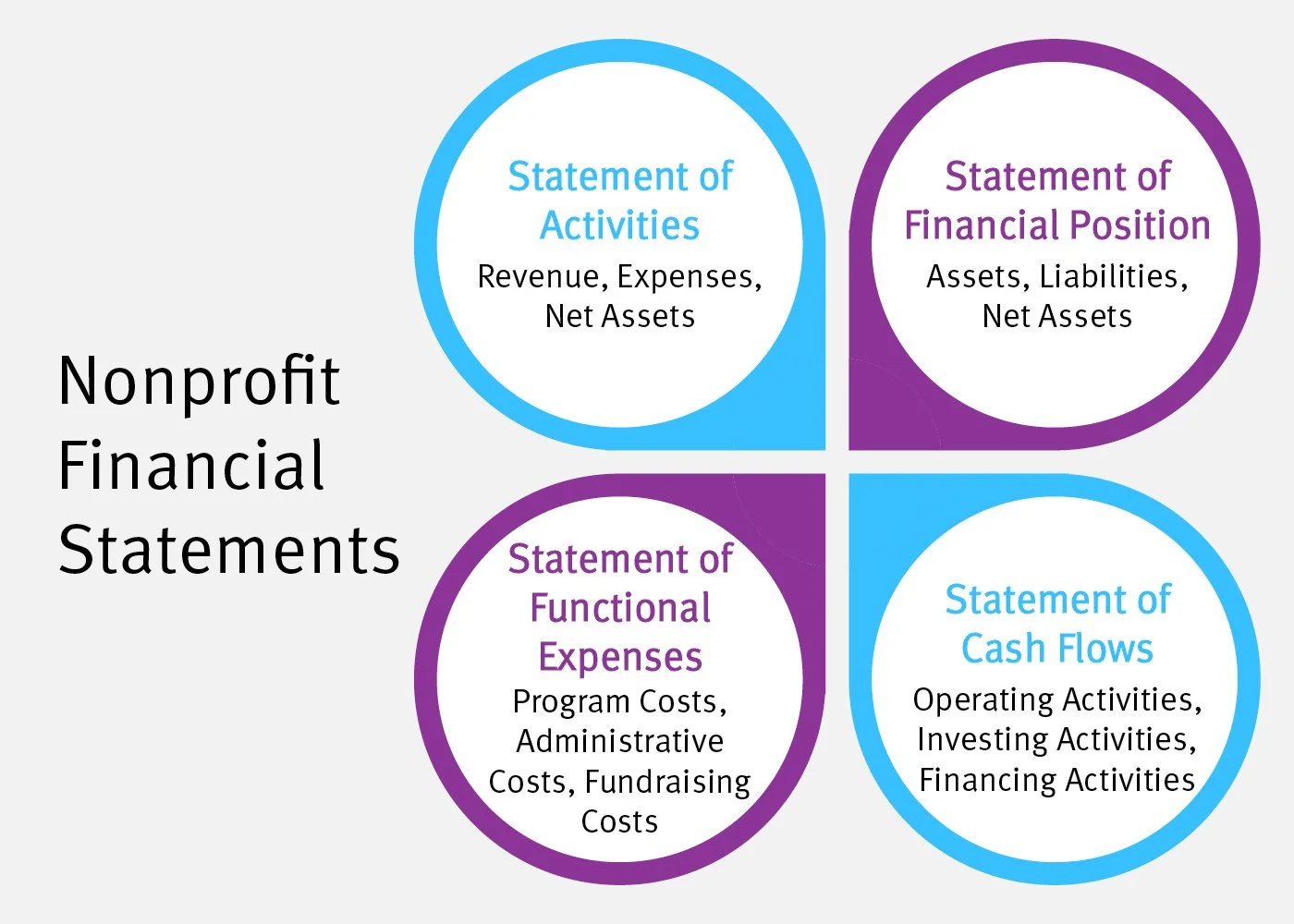

Although your chart of accounts helps you locate your nonprofit’s financial records, its format isn’t the most conducive to drawing actionable conclusions from your stored data. This is where financial statements come in. This set of four reports organizes and summarizes financial information in various ways for easier analysis.

Your nonprofit should compile the following financial statements at the end of each year:

Statement of activities: As the nonprofit parallel to the for-profit income statement, this report breaks down your annual revenue, expenses, and change in net assets to help you evaluate your fundraising success and create more accurate budgets.

Statement of financial position: Also known as a balance sheet, this statement summarizes your organization’s assets, liabilities, and net assets to provide a snapshot of its financial health and growth potential.

Statement of cash flows: This report tracks how cash moves in and out of your nonprofit through operating, investing, and financing activities. Many organizations compile this statement monthly as well as annually for more accurate cash flow monitoring.

Statement of functional expenses: The one financial statement unique to nonprofits, this report divides your expenses into program, administrative, and fundraising categories to demonstrate how your organization’s spending furthers its mission.

In addition to supporting internal decision-making, these financial statements help your organization be transparent with its community, cultivating the necessary trust for future fundraising success. DonorSearch recommends “includ[ing] graphical representations of key financial information in the body of your annual report, then attach[ing] detailed financial statements as appendices” to accommodate various levels of financial literacy and interest in your nonprofit’s situation among its current and potential donors.

3. Create a Schedule for Tax Filing

Financial statements are also an important resource for your team to reference come tax season. Although nonprofits are generally exempt from federal income tax and most state taxes, your organization still has to file several forms to show the government that you’re using funding properly and do your due diligence as an employer. All of these forms have stringent deadlines, and filing late can result in financial penalties or even risk your nonprofit’s exempt status.

Here are a few tax deadlines your nonprofit should keep on its radar going into the new year:

Federal tax return: The Form 990 filing deadline is the 15th day of the fifth month after your organization’s fiscal year ends. If your nonprofit uses the calendar fiscal year, your Form 990 is due May 15, but make sure to note your unique deadline if not.

State-specific forms: Every state has different filing requirements for nonprofits, so you’ll need to check what forms and due dates apply to your organization. However, most states that ask for copies of nonprofits’ Form 990s have the same filing deadline as federal returns, as do California and New York (which require the additional Form 199 and Form CHAR500 respectively).

Employer tax forms: All W-2s and 1099s need to be distributed to your nonprofit’s individual employees and contractors respectively by January 31, regardless of your organization’s fiscal calendar.

As you wrap up the year’s financial management tasks, create a calendar of these tax filing deadlines so your organization can enter the new year prepared to complete these forms correctly and on time.

4. Develop a Data-Driven Operating Budget

The year-end financial process you’re likely most familiar with is budgeting. Once your records and reports are in order, referencing them will allow you to create an annual operating budget that’s grounded in real data, and therefore, will be more useful to your nonprofit.

Effective budgeting is a team effort that follows these basic steps:

Strategy. Hold a meeting with your nonprofit’s financial professionals, board committee chairs, and leaders from various departments (fundraising, development, marketing, etc.) to discuss your organization’s situation, get input from every group the budget will affect, and set spending and fundraising goals.

Drafting. Based on the strategy session and relevant data, your nonprofit’s financial controller or chief financial officer (CFO) will take the lead on outlining its revenue and expenses for the year.

Review. Once the draft budget is complete, other finance team members will read through it and suggest revisions to better align it with your organization’s needs and goals.

Approval. Finally, your CFO or controller will send the revised budget to your treasurer—the financial expert on your nonprofit’s board of directors—so they can present it to the rest of the board, who will vote on whether to make it official or send it back for additional editing.

Budgeting also shouldn’t be a set-it-and-forget-it activity. After the board approves your annual operating budget, schedule monthly meetings to review your progress and adjust your budget as needed to keep your nonprofit’s spending and fundraising on track.

Year-end financial management should work alongside fundraising to set your nonprofit up for success in the coming year. Use the best practices above to get started, and don’t hesitate to reach out to an accountant or other financial professional if you need help or have questions along the way.

This guest post was written by Jon Osterburg.

Since joining Jitasa in 2010, Jon Osterburg has helped hundreds of nonprofits around the world effectively manage their finances through tailored, outsourced bookkeeping and accounting services. He currently serves as Jitasa’s Chief Operating Officer, is a member of two nonprofit boards, and has earned a certificate for Executive Education from the Yale School of Management.

If you’ve been following Sherry a while and are ready to take your next step, here are THREE things you can do:

👣 Follow me on LinkedIn where I share insider info daily — the same lessons I teach my clients about attracting larger gen-ops dollars and diversifying revenue.

🍎 Grab FREE Guides + White Papers — download robust resources you can use to push against the sector’s misconceptions, equip your board, and shift your team into High-ROI fundraising.

📈 Work with me to diversify revenue & secure the gen-ops gifts you need to grow. If you’re a business-minded nonprofit CEO with big growth plans but need to make charitable revenue from investment-level donors a bigger part of your budget, you can apply to work with me here.